Mortgage Experience you can rely on

Trust us to help you find the right mortgage options and products for your current financial situation.

Mortgage financing can be confusing, it doesn't have to be, here's the plan.

Get started right away

The best place to start is to connect with us directly. The mortgage process is personal. Our commitment is to listen to all your needs, assess your financial situation, and provide you with a clear plan forward.

Get a clear plan

Sorting through all the different mortgage lenders, rates, terms, and features can be overwhelming. Let us cut through the noise, we'll outline the best mortgage products available, with your needs in mind.

Let us handle the details

When it comes time to arranging your mortgage, we have the experience to bring it together. We'll make sure you know exactly where you stand at all times. No surprises. We've got you covered.

Let's run some numbers.

Start by telling us where you're at in your home buying journey.

Check Out Our Team

What people that work with us are saying

Home Buyers Tips

Everything you need, all in one place.

We can help you arrange mortgage financing for these services:

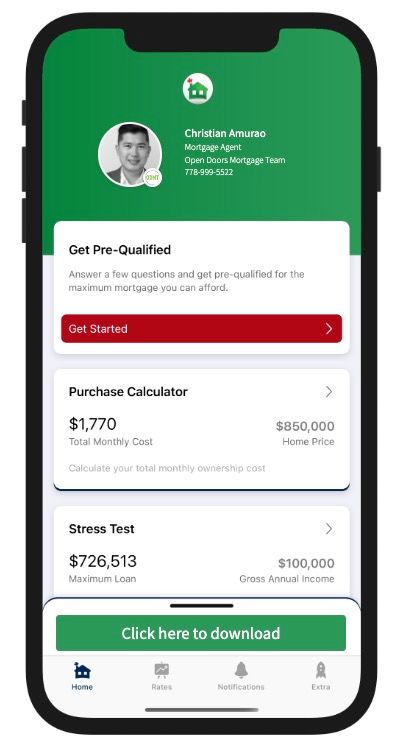

DOWNLOAD MY MORTGAGE TOOLBOX

WHAT YOU CAN DO WITH MY APP:

- Calculate your total cost of owning a home

- Estimate the minimum down payment you need

- Calculate Land transfer taxes and the available rebates

- Calculate the maximum loan you can borrow

- Stress test your mortgage

- Estimate your Closing costs

- Compare your options side by side

- Search for the best mortgage rates

- Email Summary reports (PDF)

- Use my app in English, French, Spanish, Hindi and Chinese

LET'S RUN SOME NUMBERS

OUR BLOG IS KEPT UP TO DATE SO YOU CAN STAY INFORMED!

Bank of Canada maintains policy rate at 2¼%. FOR IMMEDIATE RELEASE Media Relations Ottawa, Ontario January 28, 2026 The Bank of Canada today held its target for the overnight rate at 2.25%, with the Bank Rate at 2.5% and the deposit rate at 2.20%. The outlook for the global and Canadian economies is little changed relative to the projection in the October Monetary Policy Report (MPR). However, the outlook is vulnerable to unpredictable US trade policies and geopolitical risks. Economic growth in the United States continues to outpace expectations and is projected to remain solid, driven by AI-related investment and consumer spending. Tariffs are pushing up US inflation, although their effect is expected to fade gradually later this year. In the euro area, growth has been supported by activity in service sectors and will get additional support from fiscal policy. China’s GDP growth is expected to slow gradually, as weakening domestic demand offsets strength in exports. Overall, the Bank expects global growth to average about 3% over the projection horizon. Global financial conditions have remained accommodative overall. Recent weakness in the US dollar has pushed the Canadian dollar above 72 cents, roughly where it had been since the October MPR. Oil prices have been fluctuating in response to geopolitical events and, going forward, are assumed to be slightly below the levels in the October report. US trade restrictions and uncertainty continue to disrupt growth in Canada. After a strong third quarter, GDP growth in the fourth quarter likely stalled. Exports continue to be buffeted by US tariffs, while domestic demand appears to be picking up. Employment has risen in recent months. Still, the unemployment rate remains elevated at 6.8% and relatively few businesses say they plan to hire more workers. Economic growth is projected to be modest in the near term as population growth slows and Canada adjusts to US protectionism. In the projection, consumer spending holds up and business investment strengthens gradually, with fiscal policy providing some support. The Bank projects growth of 1.1% in 2026 and 1.5% in 2027, broadly in line with the October projection. A key source of uncertainty is the upcoming review of the Canada-US-Mexico Agreement. CPI inflation picked up in December to 2.4%, boosted by base-year effects linked to last winter’s GST/HST holiday. Excluding the effect of changes in taxes, inflation has been slowing since September. The Bank’s preferred measures of core inflation have eased from 3% in October to around 2½% in December. Inflation was 2.1% in 2025 and the Bank expects inflation to stay close to the 2% target over the projection period, with trade-related cost pressures offset by excess supply. Monetary policy is focused on keeping inflation close to the 2% target while helping the economy through this period of structural adjustment. Governing Council judges the current policy rate remains appropriate, conditional on the economy evolving broadly in line with the outlook we published today. However, uncertainty is heightened and we are monitoring risks closely. If the outlook changes, we are prepared to respond. The Bank is committed to ensuring that Canadians continue to have confidence in price stability through this period of global upheaval. Information note The next scheduled date for announcing the overnight rate target is March 18, 2026. The Bank’s next MPR will be released on April 29, 2026. Read the January 28th, 2026 Monetary Report

Thinking About Buying a Second Property? Here’s What to Know Buying a second property is an exciting milestone—but it’s also a big financial decision that deserves thoughtful planning. Whether you're dreaming of a vacation retreat, building a rental portfolio, or looking to support a family member with a place to live, there are plenty of reasons to consider a second home. But before you jump in, it's important to understand the strategy and steps involved. Start with “Why” The best place to begin? Clarify your motivation. Ask yourself: Why do I want to buy a second property? What role will it play in my life or finances? How does this fit into my long-term goals? Whether your focus is lifestyle, income, or legacy planning, knowing your “why” will help you make smarter decisions from the start. Talk to a Mortgage Expert Early Once you’ve nailed down your goals, the next step is to sit down with an independent mortgage professional. Why? Because buying a second property isn't quite the same as buying your first. Even if you’ve qualified before, financing a second home has unique considerations—especially when it comes to down payments, debt ratios, and how lenders assess risk. How Much Do You Need for a Down Payment? Here’s where the purpose of the property really matters: Owner-occupied or family use: You may qualify with as little as 5–10% down, depending on the property and lender. Income property: Expect to put down 20–35%, especially for short-term rentals or if it won’t be occupied by you or a family member. Your down payment amount can be one of the biggest hurdles—but with strategic planning, it’s often manageable. Ways to Fund the Down Payment If you don’t have the full amount in cash, you might be able to tap into your current home’s equity to help fund the purchase. Here are a few ways to do that: ✅ Refinance your existing mortgage to access additional funds ✅ Secure a second mortgage behind your current one ✅ Open a HELOC (Home Equity Line of Credit) ✅ Use a reverse mortgage (in certain age-qualified scenarios) ✅ Take out a new mortgage if your current home is mortgage-free These options depend on your income, credit, home value, and overall financial picture—another reason why having a pro in your corner matters. Second Property Strategy: It’s More Than Just Numbers This purchase should be part of a bigger financial plan—one that balances risk and reward. It’s about: Assessing your full financial health Maximizing your existing assets Minimizing your cost of borrowing Aligning your purchase with your long-term goals Ready to Take the Next Step? There’s no one-size-fits-all answer when it comes to buying a second property. That’s why it helps to talk things through with someone who understands both the big picture and the small details. If you’re ready to explore your options and build a plan to make that second property dream a reality, let’s connect. I’d love to help you take the next step with confidence.

Wondering If Now’s the Right Time to Buy a Home? Start With These Questions Instead. Whether you're looking to buy your first home, move into something bigger, downsize, or find that perfect place to retire, it’s normal to feel unsure—especially with all the noise in the news about the economy and the housing market. The truth is, even in the most stable times, predicting the “perfect” time to buy a home is incredibly hard. The market will always have its ups and downs, and the headlines will never give you the full story. So instead of trying to time the market, here’s a different approach: Focus on your personal readiness—because that’s what truly matters. Here are some key questions to reflect on that can help bring clarity: Would owning a home right now put me in a stronger financial position in the long run? Can I comfortably afford a mortgage while maintaining the lifestyle I want? Is my job or income stable enough to support a new home? Do I have enough saved for a down payment, closing costs, and a little buffer? How long do I plan to stay in the property? If I had to sell earlier than planned, would I be financially okay? Will buying a home now support my long-term goals? Am I ready because I want to buy, or because I feel pressure to act quickly? Am I hesitating because of market fears, or do I have legitimate concerns? These are personal questions, not market ones—and that’s the point. The economy might change tomorrow, but your answers today can guide you toward a decision that actually fits your life. Here’s How I Can Help Buying a home doesn’t have to be stressful when you have a plan and someone to guide you through it. If you want to explore your options, talk through your goals, or just get a better sense of what’s possible, I’m here to help. The best place to start? A mortgage pre-approval . It’s free, it doesn’t lock you into anything, and it gives you a clear picture of what you can afford—so you can move forward with confidence, whether that means buying now or waiting. You don’t have to figure this out alone. If you’re curious, let’s talk. Together, we can map out a homebuying plan that works for you.